In 2023 and beyond, leveraging digital banking transformation will continue to be a prominent.

How?

Well, technology, like its influence on other emerging markets, is gradually transforming the field of financial services in every manner. However, the sector has a long road ahead, as banks are still experimenting digitally.

Meanwhile, consumer behavior and demands have also evolved to a great extent. Gen-Z and younger generations are so inclined towards the digital transformation of Google and Apple that they want traditional banks to respond in the same way. As a consequence, conventional banks feel compelled to provide unique and effective digital solutions to assure long-term industry sustainability.

What is digital banking transformation?

Digital banking innovation is a technologically enabled cultural, institutional, and functional shift. Digital transformation, in its simplest basic form, is the progression to digitized client services delivered over the Internet. In a deeper context, digital transformation entails enhancements to a variety of areas such as offers, automation systems, user experience, advanced analytics, team building, and marketing.

This technology trend defines the industry’s path, and banks must implement quality innovations into their strategy. According to Gartner, 69% of boards of directors believe that the pandemic has hastened their digital plans.

This raises a plethora of concerns about digital transformation banking sector and other commercial institutions. Let us begin by examining how the digital process in banking began, taking into account the transition from a traditional to a modern outlook.

Evolution of digital banking

Due to technological advancements and dynamically changing consumer expectations, traditional banking has brought about a paradigm shift into digital banking. Several traditional banks have observed the need to surpass their consumers’ demands and have shifted their services to the digital realm.

Why was digital transformation in banking Industry needed?

Traditional banking has been widely practiced for years, with people visiting banks to meet their finances. It could be for collecting money, investing it, or releasing funds from one bank account to another. To fulfill their financial requirements, they had to wait in enormous lines.

This entire process did take time, and with the digitization of several sectors, banks recognized the necessity to switch to online banking processes.

Financial service providers understood that becoming digital might assist them in many ways, including improved productivity, development, and the ease it will bring users, which will result in acquiring additional potential customers.

Therefore, people are embracing the convenience of monitoring their accounts without needing to go to banks now that most banking services have moved online. A few noteworthy digital transformation examples in banking are online applications, data encryption software, chatbots, KYC, application/website optimization, and more.

What is the need of opting for digital banking transformation in 2026?

The methodology of innovative digital banking solutions is gaining traction across all sectors, regardless of end-user base or other variables.

Rising smart device adoption, enhanced internet, and requirement for high-end consumer experience are among the biggest drivers propelling the digital transformation wave, which is bringing services to the consumer’s door.

The banking industry is however one area that is witnessing such speedy transformation, allowing users to adopt bank digital banking technologies.

However, an effective digitalization route in the finance industry is predicated on the critical variables mentioned below.

- Clients are Crucial

- Constant Growth

- Streamlined Procedures

- Modern Infrastructure

- Operating Models

- Leveraging the Power of Data

Clients are Crucial

Why would banking firms transition to digital platforms? In today’s rapidly changing industry trends, smooth quality service, high-end UX, tailored product experience, accountability, and confidentiality are at the heart of consumer pleasure. To be successful in this highly competitive environment, businesses must adopt a ‘customer-first’ strategy.

Altering operational strategy, incorporating digital banking technologies into service offerings, improving customer relationship processes, and more, are the activities that not only improve your service quality but also increase client involvement with your business, which is the primary driver of any business’s success.

Constant Growth

Continuous improvement demands a streamlined innovation delivery pipeline based on agile practices. The pipeline should be so powerful that it can effortlessly track evolving market dynamics, embrace new solutions, and enable quick feedback loops to adapt products for improvements. This cycle adds naturally to on-demand service delivery, continuous invention, and continual improvement, resulting in a shorter time-to-market.

Streamlined Procedures

Most digital banking operations have now become streamlined with digital banks. Refining functions also conserves resources and time while allowing internal banking departments to operate more effectively. It will also draw additional consumers to the bank because of its simplified operations.

Modern Infrastructure

The underlying infrastructure is vital in enabling the sharing of information essential in the front-end journey to digital transformation. As a result, it is critical to modernize your old infrastructure to facilitate initiatives for digital transformation.

What we must realize is that the globe has become increasingly interconnected, and transformation is taking place at a faster pace than ever before, thanks to digital techniques that have supported digitalization.

In this regard, microservices, APIs, and DevOps might be advantageous for continuous deployment and delivery, resulting in quicker rollouts.

Operating Models

Customers now require a varied experience, a combination of never-before-seen digital user experiences in terms of ease and efficiency, as well as the personal use and sense of the product. This is attainable by transforming the firm into three distinct digitization technology models:

> Digital as a Business – At the Management Level

> Digital as a New Line of Business – At the next level, a dedicated digital division will handle all digital activities

> Digital Native – Company equipped with its technological stack that focuses on clients directly

These are the diverse types of digital business transformation models accessible. However, choosing the proper one necessitates due diligence and skill.

Leveraging the Power of Data

Banking organizations must appreciate the significance of data, as well as related technologies and assets, in advancing productivity and profitability. They must consider more information technology approaches to identify and track client mindsets. This enables them to provide the most relevant items that meet the needs of their customers.

This will also enable them to gain crucial market insights that would aid them in improving service offerings, user experience, and client relationships.

Benefits of digital banking transformation

As we have aforementioned, innovative digital banking solutions encompasses a lot more than quick transactions and Internet banking. Banking transformation creates numerous additional options for small and midsize enterprises, large organizations, and similar institutions. The below advantages have resulted from the digitization of banks-

> Improved security on all levels of data handling

> Quick operation and lower waiting times

> Efficient analysis and risk management for banking operations

> AI predictive capabilities

> Customization and personalization

> Automation of tasks

As we stand on the cusp of a new era in banking, it is clear that digital transformation will play a significant role in shaping the future of banks. With careful planning and responsible use, digitization has the power to revolutionize the banking landscape in ways we can only begin to imagine.

Digital transformation examples in banking

Have you ever wondered how digital banking evolution has changed the way we manage our money? It's truly amazing how technology has revolutionized traditional banking practices, offering us convenience, speed, and security. Today, I want to take you on a journey to explore some fascinating examples of digital banking that have emerged in recent years. We'll dive into the innovative features and benefits that these advancements bring to customers like you and me.

Mobile Banking Apps

Let's start with something you probably use regularly – mobile banking apps. Think of apps like ICICI, SBI Bank, or Indian Bank. They're like pocket-sized banks, providing a wide range of features to make your life easier. From checking your account balance to transferring funds, paying bills, or even managing your finances, these apps are designed to give you access to your accounts whenever and wherever you need them.

Digital Wallets

Have you ever imagined leaving your physical wallet at home and still being able to make payments? Well, digital wallets have made that possible! Services like Apple Pay, Google Pay, and Samsung Pay allow you to store your debit and credit card information securely on your smartphone. Just a simple tap on a payment terminal, and voila! You've made a contactless payment, keeping your transactions both convenient and secure.

Online-only Banks

Now, let's talk about a new breed of banks – online-only banks, also known as virtual or neo-banks. These banks operate entirely online, meaning no physical branches. Companies like Chime, Revolut, and N26 offer a wide range of banking services, from checking and savings accounts to loans and money management tools. The best part? They often provide competitive interest rates, low fees, and a seamless digital experience, perfect for those who embrace the convenience and cost-effectiveness of online banking.

Peer-to-Peer (P2P) Payments

Have you ever been out with friends, splitting a bill, and realized you didn't have cash? No worries! Peer-to-peer payment platforms like PayPal, Paytm, and GooglePay have got your back. These platforms enable you to send and receive money instantly, just by using your email address or mobile number. They've made splitting bills, sharing expenses, and sending money to loved ones as easy as a few taps on your phone.

Open Banking

Let's talk about something that promotes competition and innovation in the banking industry – open banking. This concept allows you to securely share your financial data with authorized third-party providers. Companies like Plaid and Yodlee provide APIs and data aggregation services that empower developers to create amazing financial management tools, budgeting apps, and lending solutions. Open banking puts you in control and helps you access personalized financial services tailored to your needs.

Robo-Advisors

When it comes to investing, technology has brought us robo-advisors. Think of Betterment and Wealthfront as your digital investment assistants. These platforms use advanced algorithms to offer personalized investment advice and automated portfolio management. They're like having a financial advisor in your pocket, guiding you toward your financial goals with lower fees compared to traditional advisors. Robo-advisors have made investing more accessible and simplified for a broader audience.

So, there you have it – a glimpse into the exciting world of digital banking! These examples are just the tip of the iceberg. As technology continues to evolve, we can expect even more amazing advancements in areas like artificial intelligence, blockchain, and cybersecurity. The future holds personalized and secure banking experiences that will make managing our finances easier and more efficient than ever before.

Future of digital transformation in banking

Welcome to the future of digital banking, where the financial landscape is undergoing a remarkable transformation. As technology progresses at an astounding pace, banks and crypto wallets are converging to shape a new era of financial services. In this article, we'll explore the exciting developments that lie ahead, paving the way for a convenient, secure, and personalized banking experience like never before.

Artificial Intelligence and Machine Learning

Imagine having your very own virtual banking assistant available around the clock. With the advancements in Artificial Intelligence (AI) and Machine Learning (ML), banks are embracing intelligent chatbots and virtual assistants to provide instant support and guidance to customers. These AI-powered systems will not only answer queries but also analyze vast amounts of data to offer personalized financial recommendations and insights tailored to your unique needs.

Enhanced Security Measures

Security is a top priority in the digital banking landscape, and as cryptocurrencies gain popularity, the need for robust security measures becomes even more critical. In the future, expect to see biometric authentication methods like fingerprint and facial recognition becoming standard across both traditional banking and crypto wallet platforms. Additionally, the application of blockchain technology will provide tamper-proof transaction records, ensuring a high level of security and reducing the risk of fraud.

Open Banking and Collaboration

Open banking initiatives are breaking down barriers between banks and fintech companies, resulting in exciting collaborations. This collaboration allows customers to securely share their financial data with third-party applications and services, including crypto wallets. As a result, users will have a unified view of their traditional bank accounts and crypto assets, allowing for seamless management and transfers between the two.

Personalization and Customer Experience

Gone are the days of one-size-fits-all banking services. The future of digital banking lies in hyper-personalization, where financial products and services are tailored to individual customer needs. By leveraging customer data and advanced analytics, and AI banking solutions, banks, and crypto wallets will offer targeted offers, customized recommendations, and personalized financial planning. Your banking experience will become more intuitive, adapting to your preferences across various digital channels.

Internet of Things (IoT) and Connected Devices

In the not-so-distant future, your smart devices, such as wearables, connected cars, and smart homes, will seamlessly integrate with both digital banking platforms and crypto wallets. This integration will enable you to make transactions, monitor your accounts, and receive real-time notifications wherever you are. Picture effortlessly paying for your morning coffee using your smartwatch, all while your crypto investments are being monitored and managed in real-time.

Digitization of Traditional Banking Processes

The digitization wave is not limited to just banking operations but also extends to crypto wallet functionalities. Traditional banking processes, such as paperless onboarding and digital document verification, will become the norm. Similarly, crypto wallet platforms will offer streamlined user experiences, simplifying the process of buying, selling, and storing cryptocurrencies. This shift towards digitization will result in faster, more convenient services, eliminating the hassle of manual paperwork and geographical restrictions.

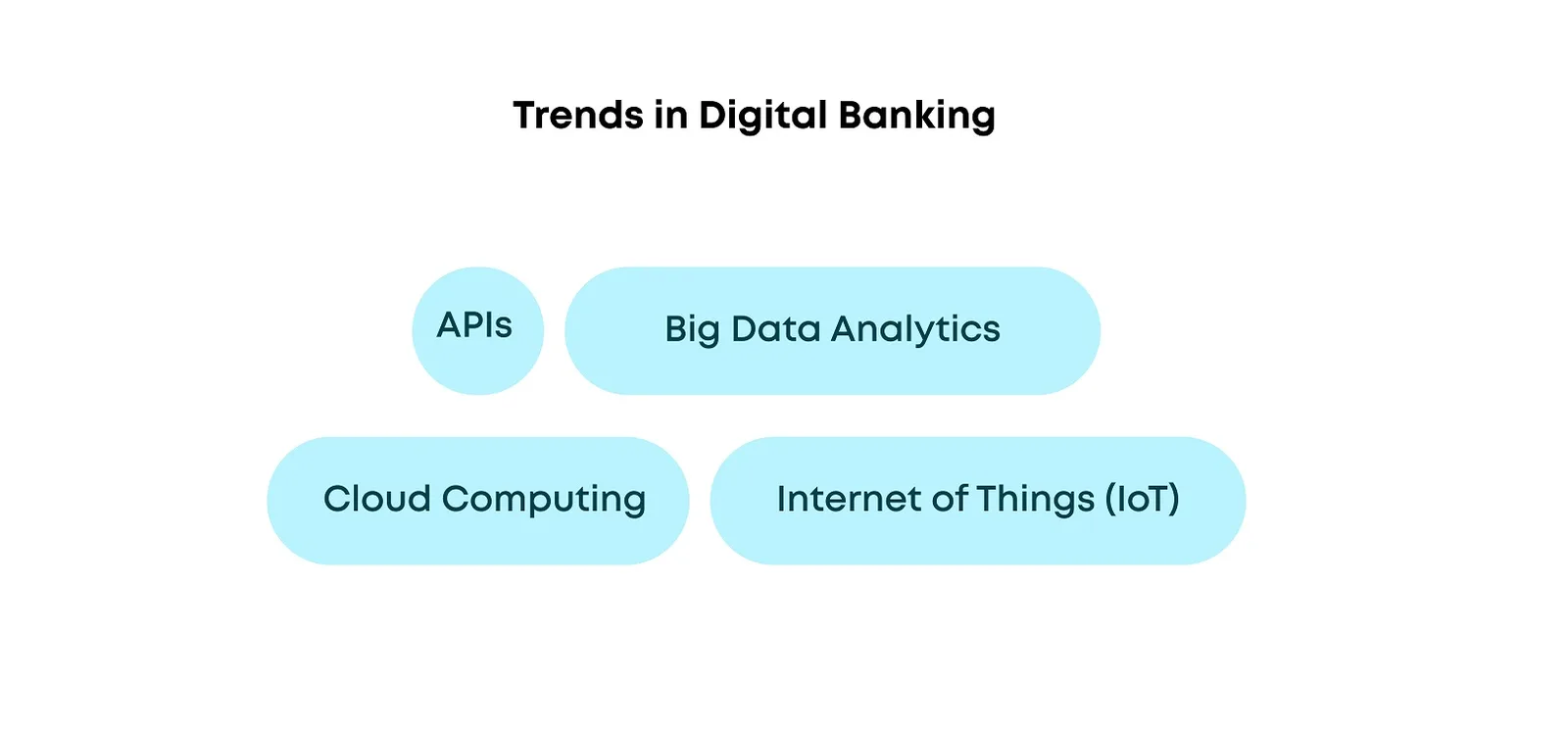

Digital banking trends 2026

We are stepping into a world where AI-powered assistants provide financial assistance, mobile apps immerse us in augmented worlds, and self-driving cars outperform people in driving.

Such breakthroughs usher in a completely new era for digital banking, redefining how consumers perceive their wealth.

A foresighted bank should remain at the forefront, embracing advancements that meet customers’ expectations for financial strength, income, trust, and privacy through a new degree of online, smartphone, and multi-services.

Even in the age of the most spectacular technologies, a slightly elevated perspective is insufficient on its own. Each bank’s future hinges on how effectively it can use innovation to focus on customer requirements, wants, and actions. So, let’s explore some of the famous digital technologies used by modern banks.

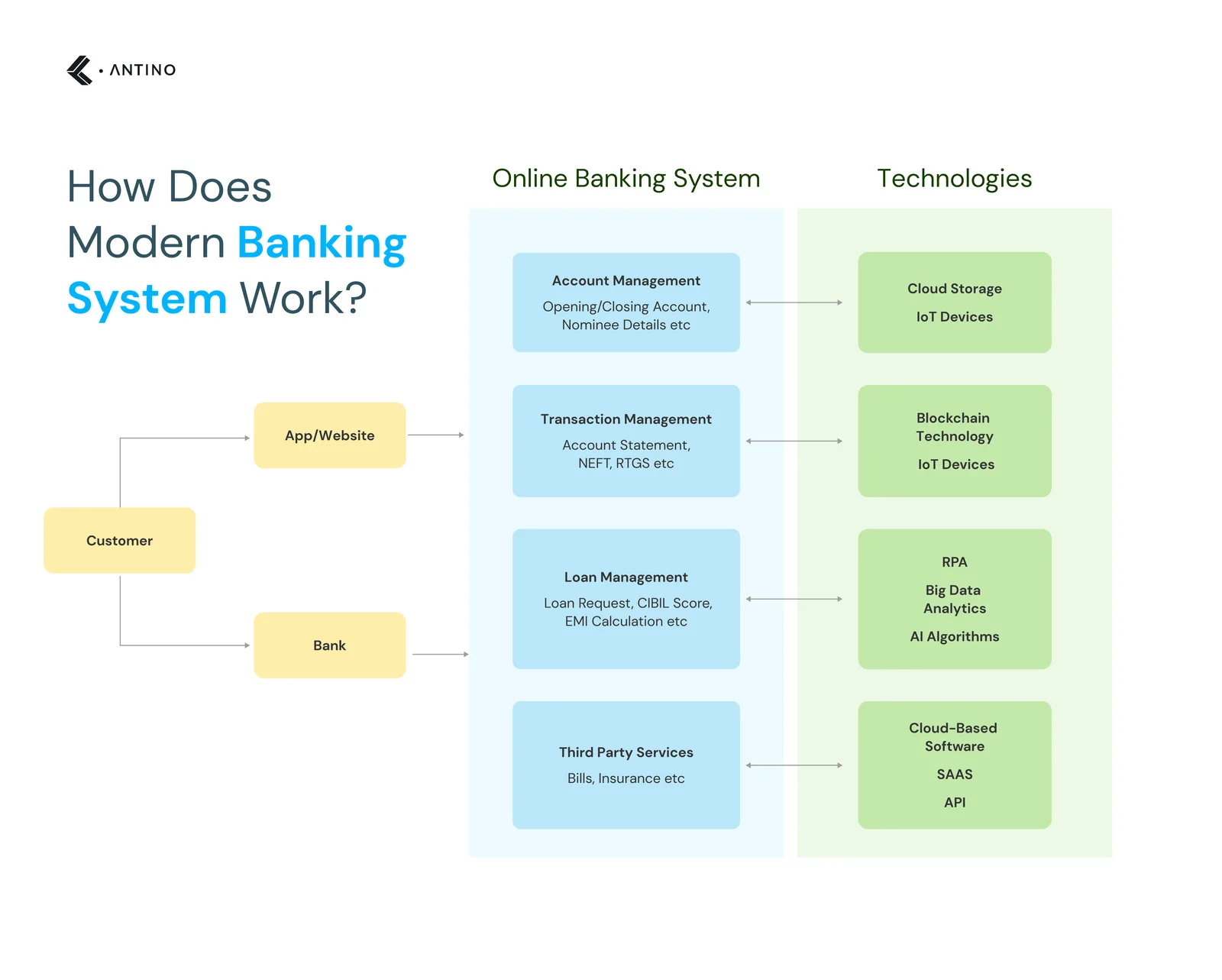

APIs

In a highly connected world, a bank’s success will be determined by its ability to create and contribute to digital networks. An important element is the bank’s capacity to integrate its goods and services, both internally as well as externally, with diverse third-party products and applications.

This is largely facilitated using APIs.

APIs (Application Programming Interfaces) enable two software systems, applications, or other resources to share information and communicate.

APIs, in other terms, allow bank services to interact with one another or with third-party goods in real-time and securely.

Cloud Computing

Banks are experiencing an influx of new rivals in the financial sector, including fintech firms, BigTech, and even non-financial entities.

To compete effectively, holders must act with flexibility and agility. Many organizations are already integrating cloud technologies into their digital marketing.

Banks can use cloud technology to preserve information and apps and access flexible computing resources on-demand over the internet.

Popular public cloud service providers such as Microsoft Azure and Google Cloud Platform provide a wide range of services to banks, enabling them to efficiently construct and scale digital innovations.

Internet of Things (IoT)

IoT is one such technology that helps in real-time data analysis by making the user experience more tailored and personalized. With real-time data analysis, IoT makes the consumer experience more personal and personalized.

Customers may make cashless transactions in seconds thanks to IoT and its digital connectivity across gadgets. Furthermore, the Internet of Things has altered the financial ecosystem by integrating risk mitigation, authentication mechanisms (biometric sensors), and accessibility to various channels.

Big Data Analytics

Banks and financial institutions, with billions of customers, are undoubtedly the most data-intensive entities in the global market.

The banks that can consistently provide personalized offers and experiences for their consumers will emerge as the next victors in the digital banking game. The key to discovering what clients want and need can be found in the mountains of data obtained across various banking platforms.

Banks can only fully listen to clients and create individualized financial services that assist them by looking at the data analysis.

Banks can use data from a variety of sources, including online payments, ATM transactions, e-banking, IoT devices, client data acquired for KYC, biometric authentication, and so on.

How can Antino be your reliable partner in the era of digitalization?

A thorough strategy and qualified specialists are required to maximize the benefits of digital transformation. Get in touch with us today for modernized fintech solutions, and we will handle all aspects of incorporating digital technologies into your business. We understand the high standards in this business and have the abilities, expertise, and discipline to deliver top-quality solutions.

FAQ's

How does digital transformation affect the banking sector?

Digital transformation in the banking sector revolutionizes processes, enhances customer experiences, and promotes efficiency through technology integration.

What are the five pillars of digital transformation?

The five pillars of digital transformation encompass technology adoption, data-driven decision-making, agile operations, customer-centricity, and a culture of innovation, all of which contribute to the successful digital transformation of a bank.